One way to think about the Federal Reserve is that it does two things. It sets interest rates, and it explains interest rates. In theory, the first job matters more. In practice, financial markets have spent the last decade becoming addicted to the second one.

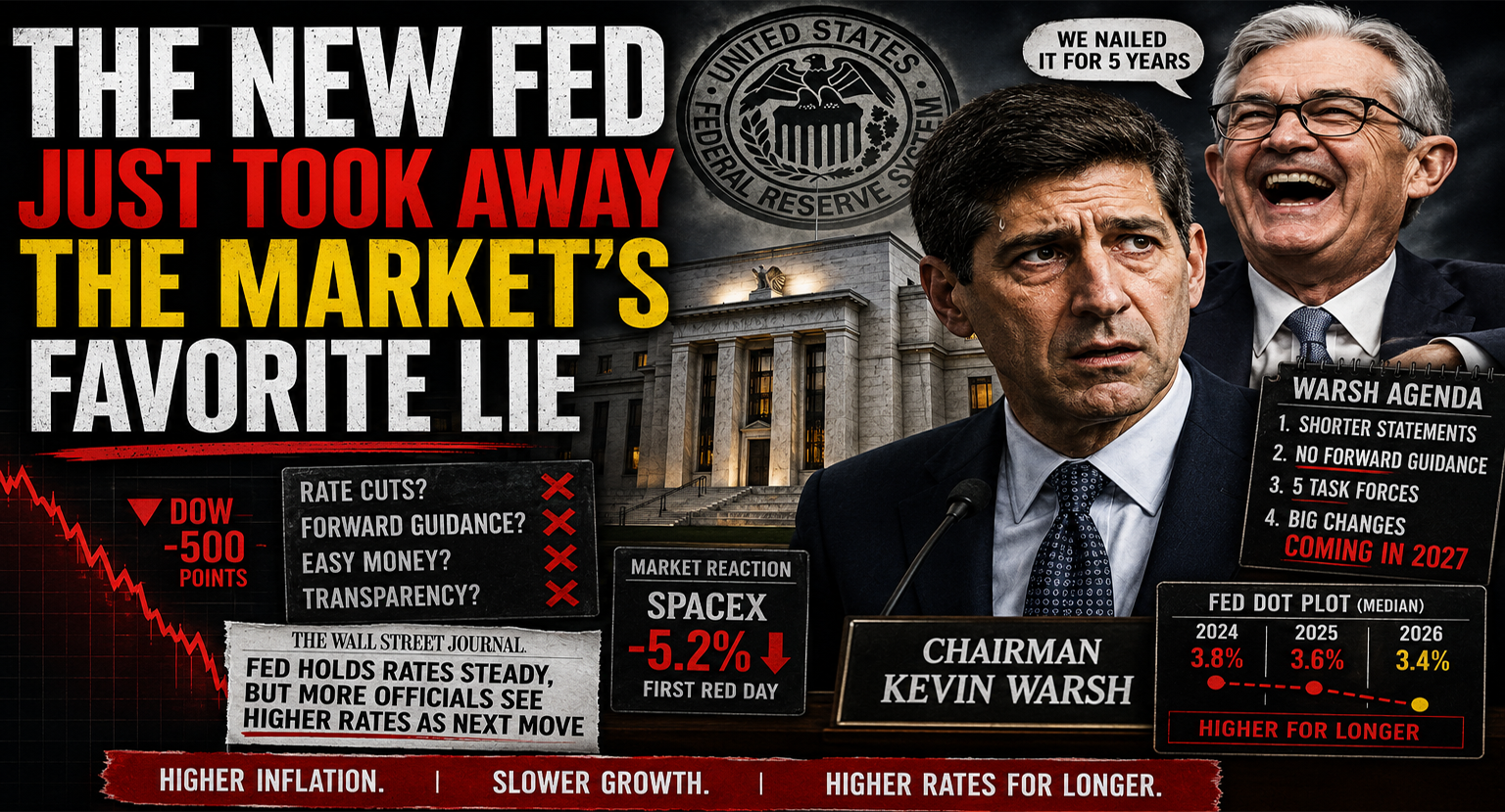

That is why Kevin Warsh’s first meeting as Fed chair was more interesting than the actual rate decision. The Fed held its benchmark rate steady at 3.5% to 3.75%, which was more or less what everyone expected. The market was not really trading on whether the Fed would cut today. It was trading on whether the Fed would help investors believe cuts were still coming later.

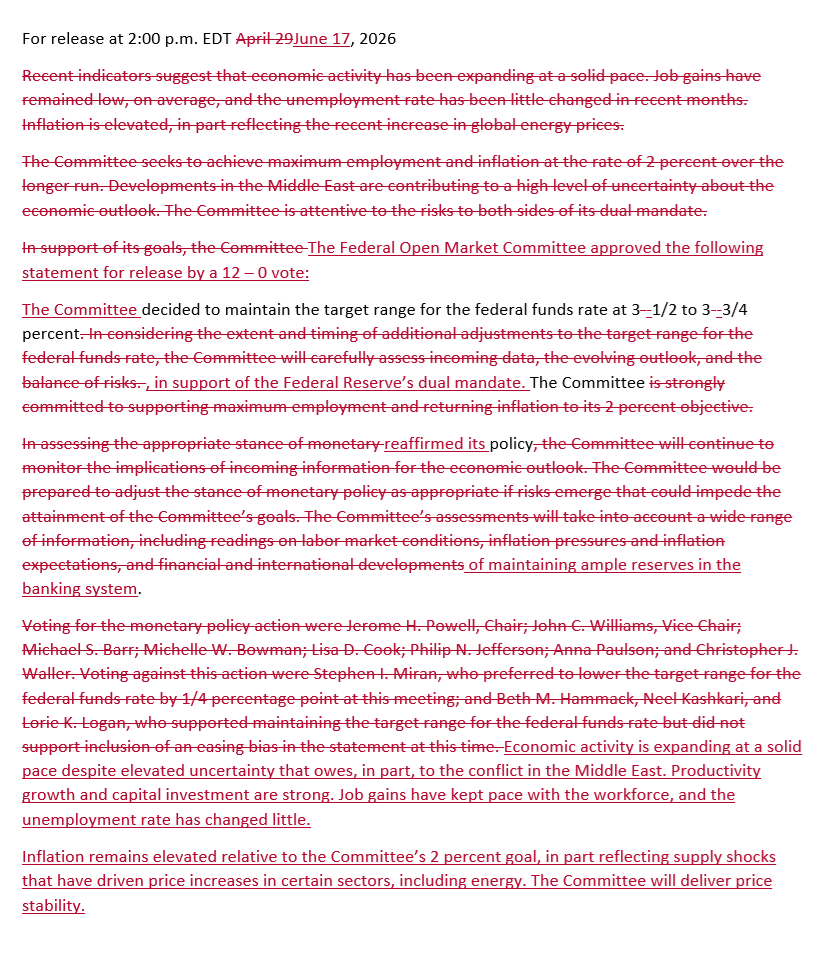

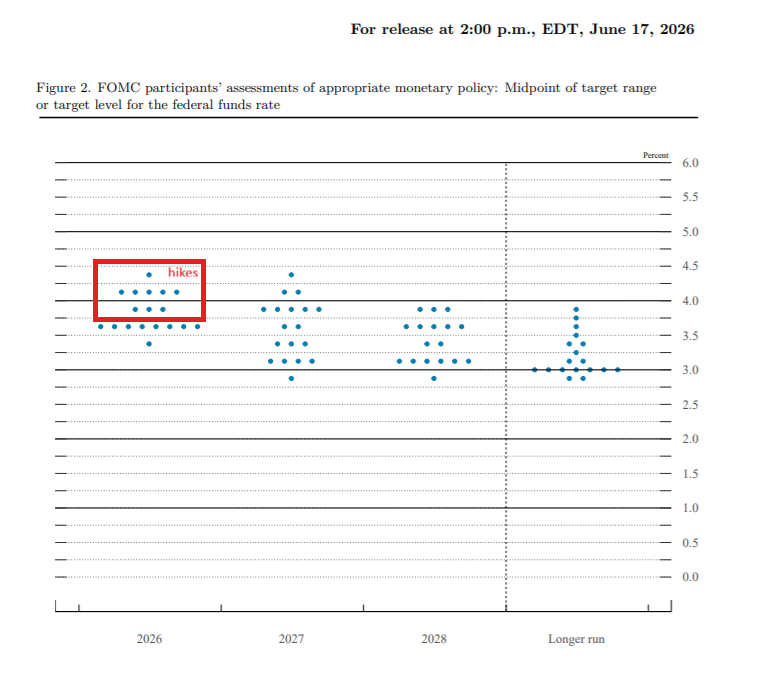

Warsh did not do that. Instead, the Fed released a shorter statement, removed some of the old explanatory language, dropped forward guidance, and signaled that officials are now much more open to raising rates than they were a few months ago. Nine of 19 officials reportedly penciled in at least one rate increase by year-end, up from zero in March. Only one official saw a cut.

That is a pretty clean message, even if the new Fed chair would apparently prefer to send fewer messages.

The rate-cut trade is not dead, exactly. Markets rarely give up their favorite fantasy all at once. But it is much harder to defend after a meeting where the Fed held rates steady, inflation forecasts moved higher, growth forecasts moved lower, and the new chair declined to submit his own rate projection. If Jerome Powell’s Fed was sometimes accused of overexplaining itself, Warsh seems interested in testing whether markets can survive with fewer subtitles.

The Fed Used to Be a Translation Service

No more forward guidance

For years, Fed communication became a product. The statement mattered. The press conference mattered. The dots mattered. The adjectives mattered. If “some” became “many,” or “firming” became “strengthening,” billions of dollars moved before anyone could admit that this was a little silly.

But it was a system. Investors understood it. The Fed would publish projections, give forward guidance, and try to reduce the risk that markets misunderstood its intentions. Sometimes this worked. Sometimes it created its own problems. If the Fed guides too much, markets stop reacting to the economy and start reacting to the guide.

Warsh seems to dislike that arrangement. His first meeting suggested a Fed that wants statements to be shorter, guidance to be less explicit, and markets to spend more time looking at incoming data rather than decoding the central bank’s tone. In a narrow institutional sense, there is a case for this. Central bankers do not actually know the future. Pretending to know the future can be expensive.

The problem is that investors prefer their uncertainty pre-digested. A less talkative Fed does not remove uncertainty from the market. It relocates it. Instead of getting a central-bank map, investors now get a stack of inflation data, employment data, oil prices, Treasury yields, and geopolitical headlines, and are told to make their own map.

That may be healthier. It is not friendlier.

Higher Inflation and Slower Growth Is the Bad Version

Trump surprised by no rate cuts

The awkward part is that Warsh is changing the communication style at a bad time. This would be easier if inflation were falling cleanly toward 2% and growth were strong enough that nobody had to worry. Then the Fed could be boring, and markets could go back to pretending every risky asset deserves a higher multiple.

That is not the setup.

The Fed is dealing with inflation that is still above target, new pressure from energy prices tied to the Middle East conflict, strong capital spending in some parts of the economy, and a consumer that does not feel nearly as good as the headline numbers suggest. The Fed can say economic activity is expanding at a solid pace, and that may be true at the aggregate level. It is also true that higher prices have been around long enough that people are no longer interested in hearing that inflation is improving slowly.

No idea why prices are higher?

This is the bad combination: inflation is too high, growth projections are softer, and rates are not coming down. You do not need to call it stagflation to see why markets dislike it. The clean playbook is gone. If growth is weak and inflation is low, the Fed can cut. If growth is strong and inflation is high, the Fed can hike. If growth is slowing while inflation stays sticky, every policy choice looks ugly.

That is the situation Warsh inherited, and his first meeting made clear that he is not interested in solving it by giving Wall Street comforting language.

Borrowers Do Not Get the Luxury of Fed Semantics

For normal borrowers, the distinction between “hold,” “hawkish hold,” and “possible hike later” is less interesting than the monthly payment. Credit cards remain expensive. Auto loans remain expensive. Small-business debt remains expensive. Mortgage rates track longer-term Treasury yields, and those yields have been moving in the wrong direction for anyone hoping housing would suddenly become affordable again.

This is why the Fed’s communication shift matters outside trading desks. A less transparent Fed can make rate volatility worse. If markets have to infer more from every inflation print or jobs report, long-term yields can move harder on each new data point. That filters into mortgage rates and corporate borrowing costs even if the Fed itself does not touch the policy rate.

In other words, the Fed can hold steady and still make financial conditions tighter if investors decide the next move might be up. That appears to be what happened after Warsh’s first meeting. The rate was unchanged, but the market heard a different Fed.

It heard a Fed that is done promising relief.

The AI Trade Has a Discount-Rate Problem

This also matters for the most speculative parts of the stock market. Bubble stocks do not just need good stories. They need low discount rates, or at least the belief that low discount rates are coming back.

SpaceX, AI infrastructure names, and every other company trading on profits that are supposed to arrive years from now are especially sensitive to this shift. If rates stay higher for longer, or if investors start pricing even a small chance of hikes, then future profits are worth less today. That is not a moral judgment. It is just math.

This is where the Fed meeting becomes a stock-market story. The market has been willing to pay aggressively for distant growth because it believed the Fed would eventually make money cheaper again. Warsh did not confirm that belief. He made it harder to price.

A transparent hawkish Fed is annoying. An opaque hawkish Fed is worse. At least with the first one, investors know what they are fighting. With the second, every data release becomes a miniature Fed meeting.

The Fed Put Is Still There, Just Farther Away

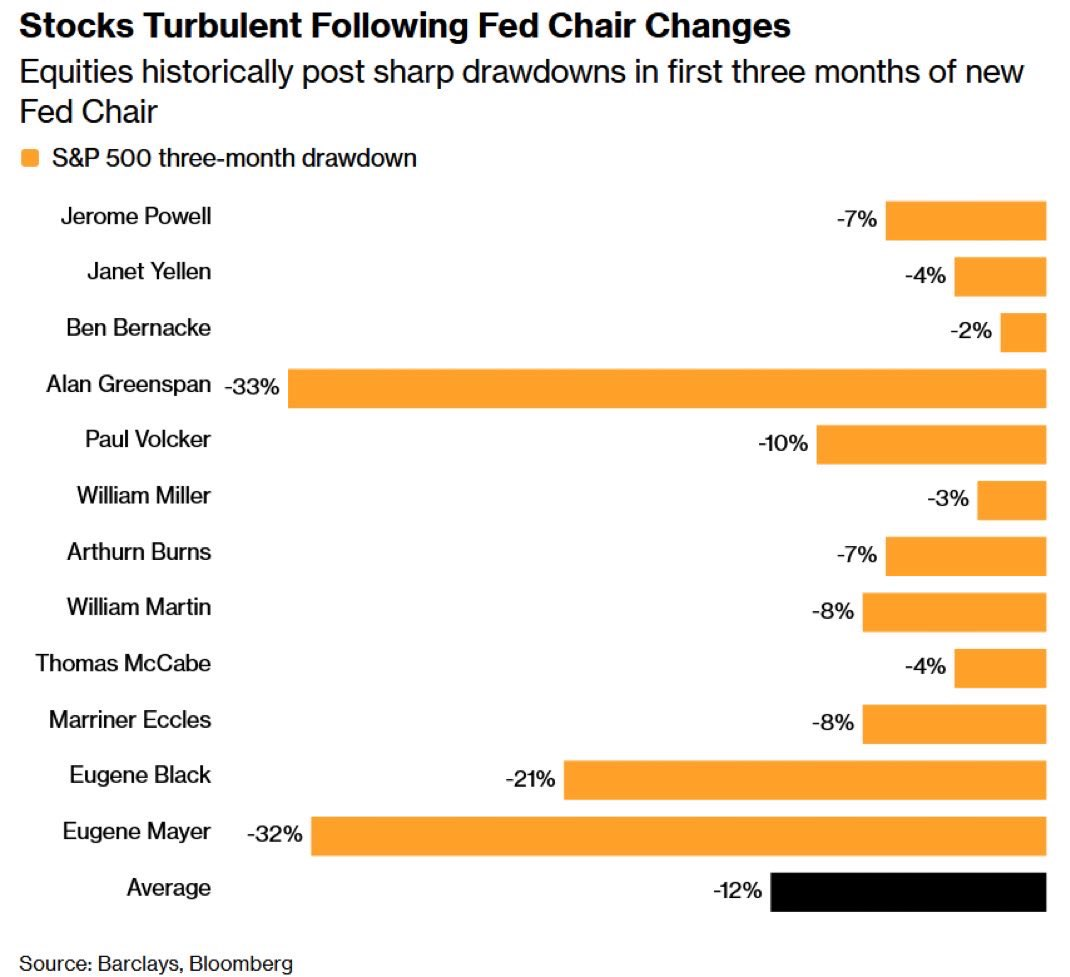

Nobody should overstate this. Warsh is not trying to crash the market. The Fed did not hike. The economy is not falling apart. Inflation is not back at 1970s levels. A soft landing is still possible in the technical sense that almost anything is possible until it is not.

But the tone changed. The market came into this year expecting a friendlier Fed, or at least a Fed that would keep hinting at future relief. Warsh’s first meeting gave investors something else: fewer hints, higher inflation forecasts, softer growth expectations, and a committee that is suddenly split between holding rates and raising them.

That is a very different world from the one risk assets wanted.

The old market story was that the Fed put still sat under every dip. If stocks fell hard enough, the Fed would eventually show up with easier money and careful words. The new story is less comforting. The put may still exist, but it is lower, harder to locate, and apparently comes without forward guidance.

That is a problem for investors who were counting on the Fed to rescue the trade before the economy forced them to read the fine print.

Warsh is asking markets to live with less guidance at the exact moment inflation is higher, growth is softer, and the next rate move might be up.

That is not a soft landing.

It is a landing without runway lights.