Advertising Disclosure: Gunnison Copper Corp. is an advertising client of SilverWars. SilverWars has received US $36,000 from Gunnison Copper Corp. under an advertising, sponsored content, and distribution agreement that includes this article. This article was prepared by SilverWars using public market sources, Gunnison Copper public disclosure, and SilverWars’ own market analysis. It is for informational and educational purposes only. It is not investment advice, not a recommendation to buy or sell any security, and not an offer or solicitation.

Copper has become the metal beneath almost every strategic conversation.

Data centers need it. Power grids need it. Defense electronics need it. The industrial world keeps rediscovering the same material under different names: electrification, AI, reindustrialization, national security, energy resilience.

But much of the public copper conversation still stops too early.

It stops at the mine gate.

That is the simple version of the story: find more copper, permit more mines, build more supply. The harder version begins one layer deeper. Mineralized material does not become copper cathode by declaration. It needs infrastructure. It needs power. It needs rail. And in heap-leach and SX/EW copper production, it needs chemistry.

Sulfuric acid is not a side chemical in that process. It is one of the industrial inputs that helps move copper into solution before SX/EW processing produces finished cathode.

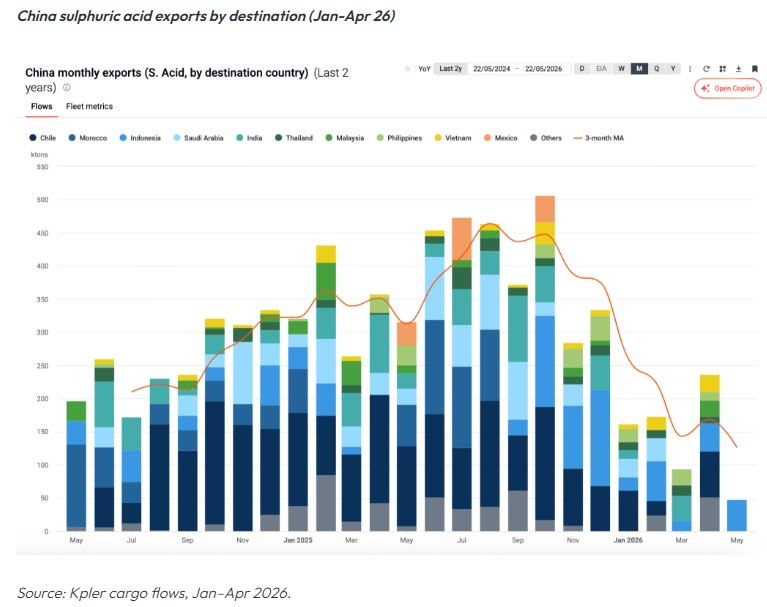

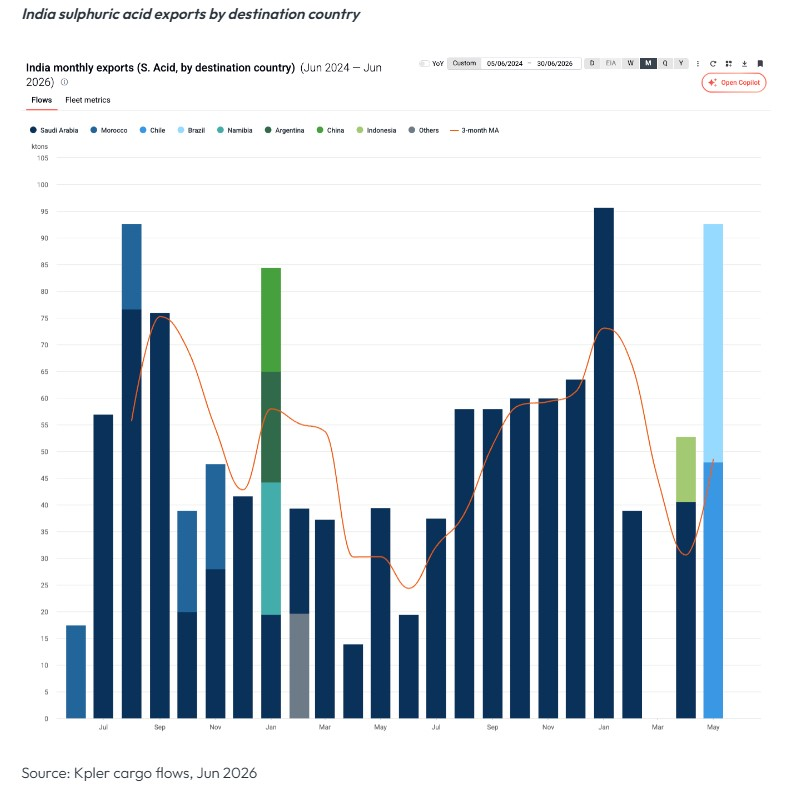

That is why the current sulfuric acid disruption deserves more attention than it has received. Reuters reported that Chinese sulfuric acid shipments to Chile fell to zero in March 2026, compared with 31,870 metric tons in February 2026 and 151,268 metric tons in March 2025. Chile matters because it is the world’s top copper-producing nation, and Reuters reported that the country depends on imported sulfuric acid for copper leaching, with 37% of those imports coming from China.

At the same time, Platts, part of S&P Global Energy, assessed sulfuric acid CFR U.S. Gulf at $400 per metric ton on May 6, up from $155 per metric ton on February 25.

The signal is larger than one country, one route, or one chemical market. A reagent bottleneck can become a metal bottleneck. The chain breaks at the link few people were watching.

“Copper is the metal everyone talks about. Acid is the control point fewer people understand,” said Craig Hallworth, President and CEO of Gunnison Copper. Hallworth was promoted to President and CEO effective May 15, 2026, according to Gunnison’s public disclosure.

That is the right way to frame the moment. Copper security is no longer only about who has resources in the ground. It is about who can turn those resources into usable metal when shipping, chemicals, power, and processing capacity are under stress.

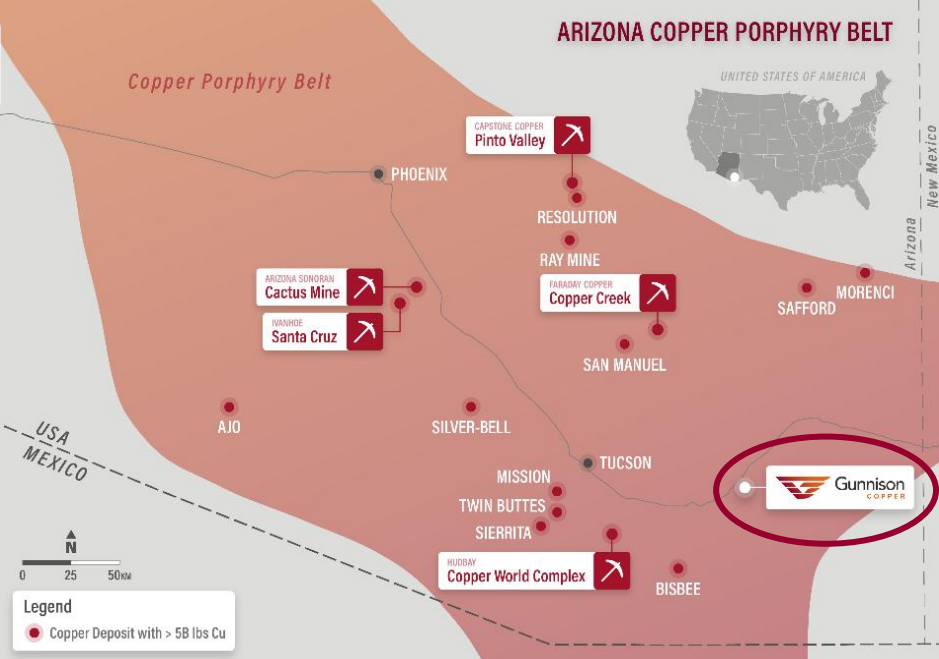

Gunnison Copper’s flagship Gunnison Project in Arizona is relevant because the design described in its 2026 Preliminary Economic Assessment does not treat those layers as afterthoughts. Gunnison’s project page describes the Gunnison Project as an open-pit, heap-leach and SX/EW operation designed to produce LME Grade A copper cathode directly on site, with onsite power, rail, and water in place.

The 2026 PEA also includes an acid plant with capacity reduced from 3,000 to 2,700 tons per day of acid production, and the PEA price deck assumes purchased sulfuric acid at $210 per ton if acid is required above the acid plant’s capacity. Gunnison also states that the acid plant generates electricity equivalent to a 26 MW power plant for use in the mine and process plant.

The Gunnison Project PEA is preliminary in nature and includes Inferred Mineral Resources that are considered too speculative geologically to have the economic considerations applied to them that would enable them to be categorized as mineral reserves. There is no certainty that the conclusions reached in the PEA will be realized. Mineral Resources that are not Mineral Reserves do not have demonstrated economic viability.

That does not make any project immune to global markets. It does something more practical. It shows a project design that recognized the vulnerability before the vulnerability became fashionable.

“A domestic copper strategy cannot stop at the mine gate. It has to include reagents, rail, power, processing, and finished cathode,” Hallworth said.

The timing matters. Copper was added to the final 2025 U.S. Critical Minerals List, and the U.S. Geological Survey estimated U.S. copper net import reliance at 57% of apparent consumption in 2025. But a critical-minerals list is not a supply chain. It is a warning label attached to an unfinished system.

A real copper strategy has to follow the metal through the whole industrial path. It has to ask where the reagent comes from. How the cathode is made. Whether power is available. Whether rail can move inputs and outputs. Whether downstream processors are ready. Whether defense, data-center, grid, and manufacturing buyers can trace the material back to a domestic source.

Gunnison is not entering that conversation from zero. The company has disclosed that its Johnson Camp Asset is in production, fully funded and supported by Nuton LLC, a Rio Tinto venture, with a ramp-up path toward nameplate capacity of 25 million pounds of finished copper cathode annually.

Gunnison has also disclosed a Rio Tinto, AWS, and Gunnison collaboration under which Amazon Web Services will use the first Nuton copper ever produced in components of its U.S. data centers. Data centers use copper in electrical cables and busbars, transformer and motor windings, printed circuit boards, and processor heat sinks.

That operating context gives the larger Gunnison Project a different kind of relevance. It is not only a future mine concept competing for attention in a crowded copper market. It is part of a district-scale Arizona platform already being built around finished domestic cathode.

The capital question, then, is not simply whether America needs more copper.

It does.

The better question is whether strategic capital understands where copper resilience is actually built.

It is built before the cathode comes off the strip. It is built in the chemistry, the rail, the power, the leach pads, the SX/EW plant, the operating permits, the technical plan, and the buyer pathway.

America needs copper. The projects that matter now are the ones designed for the chain that makes it.

Additional Disclosure and Cautionary Statements: Gunnison Copper Corp. is an advertising client of SilverWars. SilverWars has received US $36,000 from Gunnison Copper Corp. under an advertising, sponsored content, and distribution agreement that includes this article. This article was prepared by SilverWars using public market sources, Gunnison Copper public disclosure, and SilverWars’ own market analysis. It is for informational and educational purposes only. It is not investment advice, not a recommendation to buy or sell any security, and not an offer or solicitation. Readers should review Gunnison Copper’s public filings, technical reports, risk factors, and cautionary statements, and should consult their own financial, legal, tax, and investment advisers. SilverWars has not independently verified Gunnison Copper’s technical disclosure.

Scientific and technical information in this article is summarized from Gunnison Copper’s public disclosure. The Gunnison Project PEA is preliminary in nature and includes Inferred Mineral Resources that are considered too speculative geologically to have the economic considerations applied to them that would enable them to be categorized as mineral reserves. There is no certainty that the conclusions reached in the PEA will be realized. Mineral Resources that are not Mineral Reserves do not have demonstrated economic viability.

This article may contain forward-looking information based on Gunnison Copper’s public disclosure, including statements regarding project design, intended infrastructure, potential production, processing plans, supply-chain positioning, financing relevance, and strategic importance. Forward-looking information is subject to risks, uncertainties, and assumptions, and actual results may differ materially.