Advertising Disclosure: Gunnison Copper Corp. is an advertising client of SilverWars. SilverWars has received US$36,000 from Gunnison Copper Corp. under an advertising, sponsored content, and distribution agreement that includes this article. This article was prepared by SilverWars using public market sources, Gunnison Copper public disclosure, and SilverWars’ own market analysis. It is for informational and educational purposes only. It is not investment advice, not a recommendation to buy or sell any security, and not an offer or solicitation.

The strategic-materials problem is rarely solved at the resource statement.

It is solved at the point where mineral resources become usable industrial supply.

That distinction matters. A deposit can be large, politically useful, and strategically located, yet still fail to answer the requirements of defense procurement, grid expansion, data-center construction, electrical manufacturing, or industrial resilience. The relevant question is not simply whether copper exists in the ground. It is whether copper can be converted into finished, qualified, deliverable material through a chain that can withstand stress.

A nation may identify the material it needs, but identification is not capacity. Capacity requires the full industrial sequence: mine development, reagents, water, power, rail, processing, permits, technical execution, financing, and buyers prepared to contract for output.

The copper conversation has begun to acknowledge demand. It has not yet fully adjusted to conversion risk.

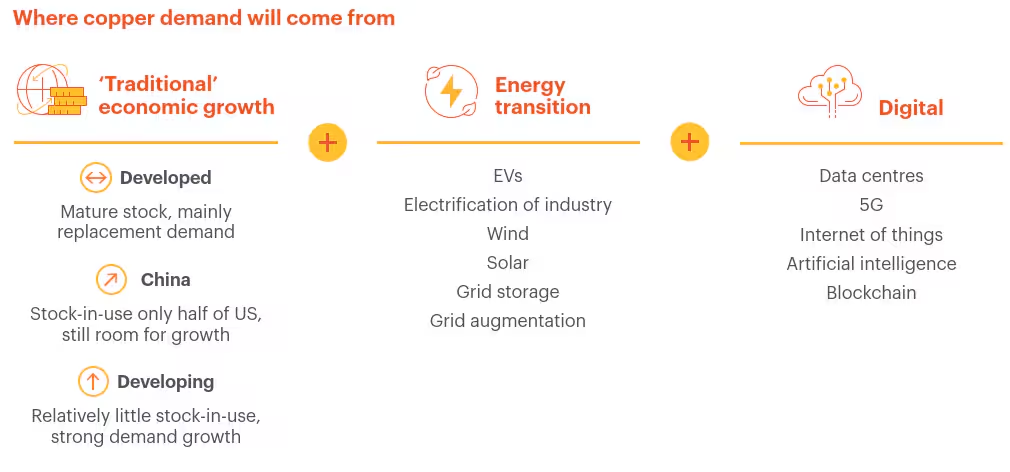

Copper is necessary for electrification, defense electronics, data centers, power infrastructure, motors, transformers, cables, busbars, thermal-management systems, and advanced manufacturing. These end markets do not consume “copper exposure.” They consume copper products that begin with reliable refined supply.

For that reason, strategic copper capital should be evaluated through a more practical lens: which projects are designed to produce usable domestic cathode, and which buyers are prepared to secure it before the next shortage is visible in price?

Offtake is where this discussion becomes serious.

An offtake agreement is not merely a financing accessory. In strategic-materials markets, it can become the bridge between industrial need and project finance. It can help a producer demonstrate demand, help a buyer secure future material, and help capital providers underwrite capacity with greater confidence. For defense, data-center, grid, and manufacturing customers, offtake can also serve a supply-assurance function that ordinary spot-market procurement cannot provide.

Recent copper and reagent-market developments show why this matters.

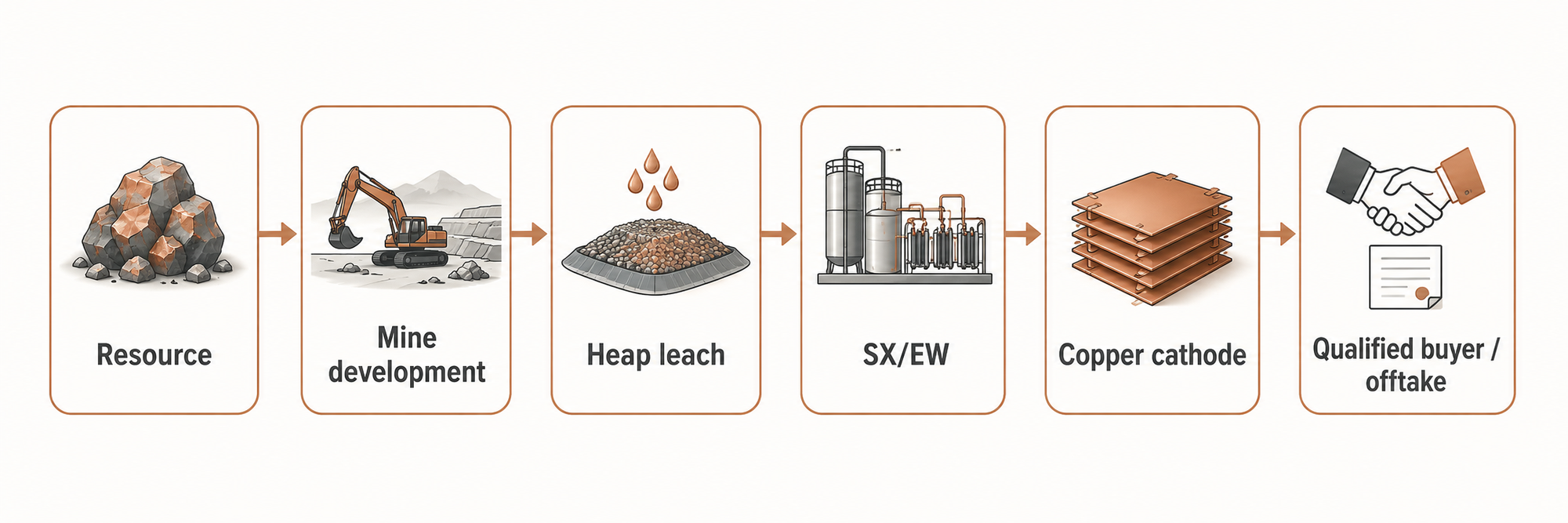

In heap-leach and SX/EW copper production, sulfuric acid is not peripheral. It is part of the process that helps move copper into solution before finished cathode can be produced. When reagent markets tighten, a copper strategy can become a chemical strategy. When logistics tighten, it becomes a rail and power strategy. When financing tightens, it becomes a contracted-demand strategy.

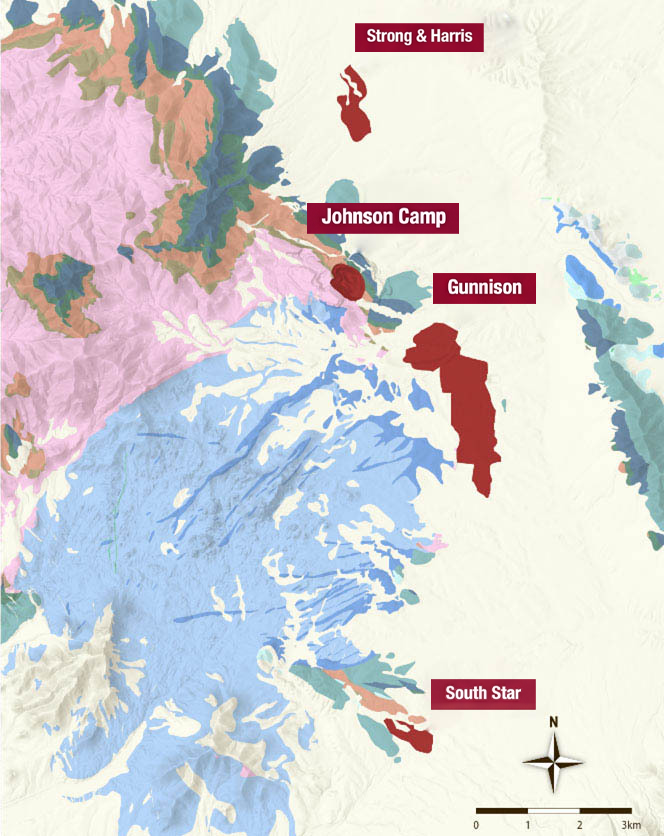

Gunnison Copper is relevant to this discussion because its Arizona platform is organized around the conversion chain, not only the resource base.

“Johnson Camp SX/EW startup imagery shows the conversion sequence from leach solution to electrolyte to copper cathode production.”

The company’s Johnson Camp Asset is already in production and, according to Gunnison disclosure, is fully funded and supported by Nuton LLC, a Rio Tinto venture, with production capacity of up to 25 million pounds of finished copper cathode annually. Gunnison has also disclosed a Rio Tinto, AWS, and Gunnison collaboration under which AWS will use the first Nuton copper produced at Johnson Camp in components for U.S. data centers.

That is not the entire answer to U.S. copper security. It is, however, a useful signal. A downstream industrial buyer is already looking beyond the abstract commodity narrative and toward source-connected copper supply.

The larger Gunnison Project carries the same strategic logic at a broader, development-stage scale. Gunnison’s public disclosure describes the project as a conventional open-pit, heap-leach and SX/EW operation intended to produce finished copper cathode on site, with direct rail access and supporting infrastructure in Arizona.

The Gunnison Project PEA is preliminary in nature and includes Inferred Mineral Resources that are considered too speculative geologically to have the economic considerations applied to them that would enable them to be categorized as mineral reserves. There is no certainty that the conclusions reached in the PEA will be realized. Mineral Resources that are not Mineral Reserves do not have demonstrated economic viability.

The caution is important. The design logic is also important.

A domestic copper platform in production at Johnson Camp, combined with a larger development-stage cathode project at Gunnison, is a different conversation than a company that only points to a stranded deposit. A project with direct rail access is different from a project still dependent on more fragile logistics. A project that incorporates reagent planning is different from one that assumes the chemical market will remain available and orderly.

“We are not designing a project that simply hopes the acid market behaves. We are designing around a vulnerability the world is now noticing,” said Craig Hallworth, President and CEO of Gunnison Copper.

If copper is now treated as a critical mineral, then the necessary policy question is not only how many pounds can be found. It is how finished domestic cathode can be produced, financed, contracted, and delivered into the supply chains that require it. This is where defense and industrial buyers have a role that is often understated.

Government can identify strategic materials. Capital can finance projects. Producers can develop assets. But the final signal often comes from buyers willing to contract for future supply. In copper, that buyer universe may include defense primes, electrical manufacturers, data-center infrastructure providers, grid equipment suppliers, critical-infrastructure contractors, and strategic stockpile or procurement channels. The value of offtake in this environment is not promotional. It is structural.

GUNNISON COPPER (GCUMF) / PR

Release Routing Desk

Appoints Bjorn Meyer as Chief Operating Officer

A buyer that waits for a mature shortage may find itself competing for the same refined supply as everyone else. A buyer that secures a domestic pathway earlier can influence the chain before it becomes crowded. For capital providers, early buyer alignment can help separate projects with strategic relevance from projects that merely benefit from a favorable commodity narrative.

This is especially important because the U.S. copper issue is not a single-mineral problem. It is a systems problem. Copper’s addition to the U.S. Critical Minerals List identifies the concern, but lists do not build capacity. Capacity requires specific projects that can turn mineral resources into usable metal and connect that metal to qualified demand.

Gunnison has also disclosed Johnson Camp’s Section 48C tax-credit selection, subject to final program requirements. That should not be read as a guarantee of future funding for the larger Gunnison Project. It should be read more narrowly: Johnson Camp has already intersected with a federal program designed around advanced energy and critical-materials industrial capacity.

“This is what domestic industrial policy should look like in practice: finished cathode on site, domestic infrastructure, and a plan for the chemistry that makes the metal,” said Craig Hallworth, President and CEO of Gunnison Copper.

Strategic copper policy should not stop at deposits. Strategic copper investment should not stop at price forecasts. Strategic copper procurement should not stop at annual purchasing cycles. The relevant unit of analysis is the chain that produces usable metal under stress.

For Gunnison, the commercial implication is straightforward. The company is positioned to be evaluated as a domestic cathode platform in production at Johnson Camp, with a larger development-stage cathode project at Gunnison. That gives it relevance to buyers who care about provenance, process resilience, and future supply assurance.

For defense and industrial customers, the question is equally direct: if copper availability becomes a binding constraint, which suppliers have the infrastructure, processing plan, and project design that can support contractable domestic output?

The next phase of copper security will likely be shaped less by slogans and more by agreements.

Policy can recognize the need. Capital can build the capacity. Offtake can connect the capacity to the buyers who cannot afford interruption.

That is where the copper chain becomes real.

Additional Disclosure and Cautionary Statements: Gunnison Copper Corp. is an advertising client of SilverWars. SilverWars has received US$36,000 from Gunnison Copper Corp. under an advertising, sponsored content, and distribution agreement that includes this article. This article was prepared by SilverWars using public market sources, Gunnison Copper public disclosure, and SilverWars’ own market analysis. It is for informational and educational purposes only. It is not investment advice, not a recommendation to buy or sell any security, and not an offer or solicitation. Readers should review Gunnison Copper’s public filings, technical reports, risk factors, and cautionary statements, and should consult their own financial, legal, tax, and investment advisers. SilverWars has not independently verified Gunnison Copper’s technical disclosure.

Scientific and technical information in this article is summarized from Gunnison Copper’s public disclosure. The Gunnison Project PEA is preliminary in nature and includes Inferred Mineral Resources that are considered too speculative geologically to have the economic considerations applied to them that would enable them to be categorized as mineral reserves. There is no certainty that the conclusions reached in the PEA will be realized. Mineral Resources that are not Mineral Reserves do not have demonstrated economic viability.

This article may contain forward-looking information based on Gunnison Copper’s public disclosure, including statements regarding project design, intended infrastructure, potential production, processing plans, supply-chain positioning, financing relevance, offtake relevance, buyer discussions, and strategic importance. Forward-looking information is subject to risks, uncertainties, and assumptions, and actual results may differ materially.