There is a quiet question sitting underneath Anduril’s recent news cycle.

It is not whether Anduril can build serious defense technology. That part is already obvious.

The better question is this: who supplies the physical inputs when Anduril starts manufacturing at the scale it is promising?

Anduril recently announced a $5 billion Series H raise, bringing its valuation to $61 billion. The company said Arsenal-1 is expected to reach high-rate production in the coming year, with manufacturing tools designed to push defense production into a new model.

That is not a normal startup milestone.

That is an industrial signal.

At the same time, Anduril has moved deeper into weapons production. The company signed a production agreement for the Surface-Launched Barracuda-500M, with delivery of associated containerized launch systems beginning with more than 60 launchers in 2027. It also won a $23.9 million U.S. Marine Corps contract to deliver more than 600 Bolt-M systems for the Organic Precision Fires-Light program.

Then add the rest of the picture.

Anduril received additional Defense Production Act Title III funding to expand domestic solid rocket motor production capacity. It is delivering battle-management capability for missile defense in the Western Pacific. Its Lattice architecture is being pushed across Army command-and-control work, connecting soldiers, sensors, vehicles, and command posts.

This is the point where Anduril’s supply-chain needs stop being theoretical.

Software can ship through code.

Weapons cannot.

Every autonomous aircraft, missile, loitering munition, sensor platform, counter-drone system, rocket motor line, and command node eventually runs into the same physical reality:

- metals

- electronics

- wiring

- connectors

- payload materials

- flame-retardant compounds

- munition-linked alloys

- industrial stockpiles

That is where two materials deserve more attention from Anduril’s own procurement and strategy teams: silver and antimony.

Silver is not just a monetary metal. It is one of the most important industrial metals in modern electronics because of its conductivity, reflectivity, and use across electrical systems.

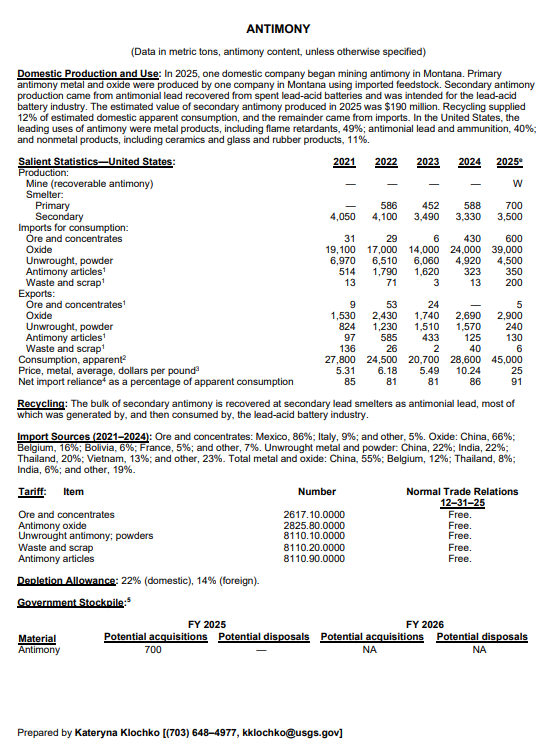

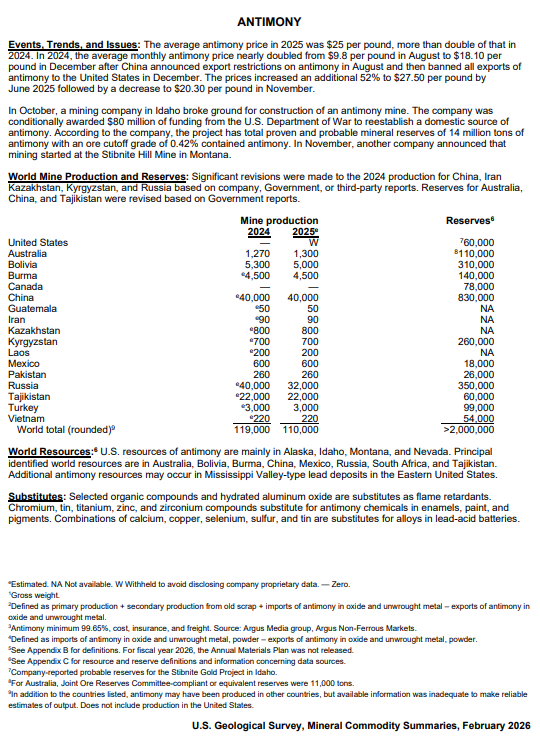

Antimony is even more direct from a defense standpoint. U.S. government data ties antimony demand to metal products, flame retardants, antimonial lead, and ammunition. China’s restrictions on antimony exports to the United States made the supply risk harder to ignore.

That should matter to Anduril.

A company trying to build the next arsenal cannot treat upstream minerals like someone else’s problem forever. At prototype volume, normal supplier channels may work. At weapons-production volume, the supply chain has to be mapped, qualified, and controlled before everyone else starts chasing the same limited material.

The Anduril Playbook Should Move Upstream

Anduril’s model is built around moving faster than the old defense primes.

That same thinking should apply to mineral supply.

The smart move is not to wait for the shortage headline. The smart move is to identify North American mining companies that can support defense-linked supply chains before every contractor starts chasing the same metals.

For Anduril, the screen is simple:

- North American production

- Defense-linked metals

- Operating assets, not just future promises

- Domestic processing potential

- Cleaner balance sheet

- Realistic offtake potential

That screen points toward Americas Gold and Silver, ticker $USAS.

Not because USAS is the biggest mining company.

Because it sits at a rare intersection: North American silver production, U.S. antimony exposure, Galena Complex ownership, and a domestic antimony processing pathway.

Why Americas Gold and Silver Fits the Moment

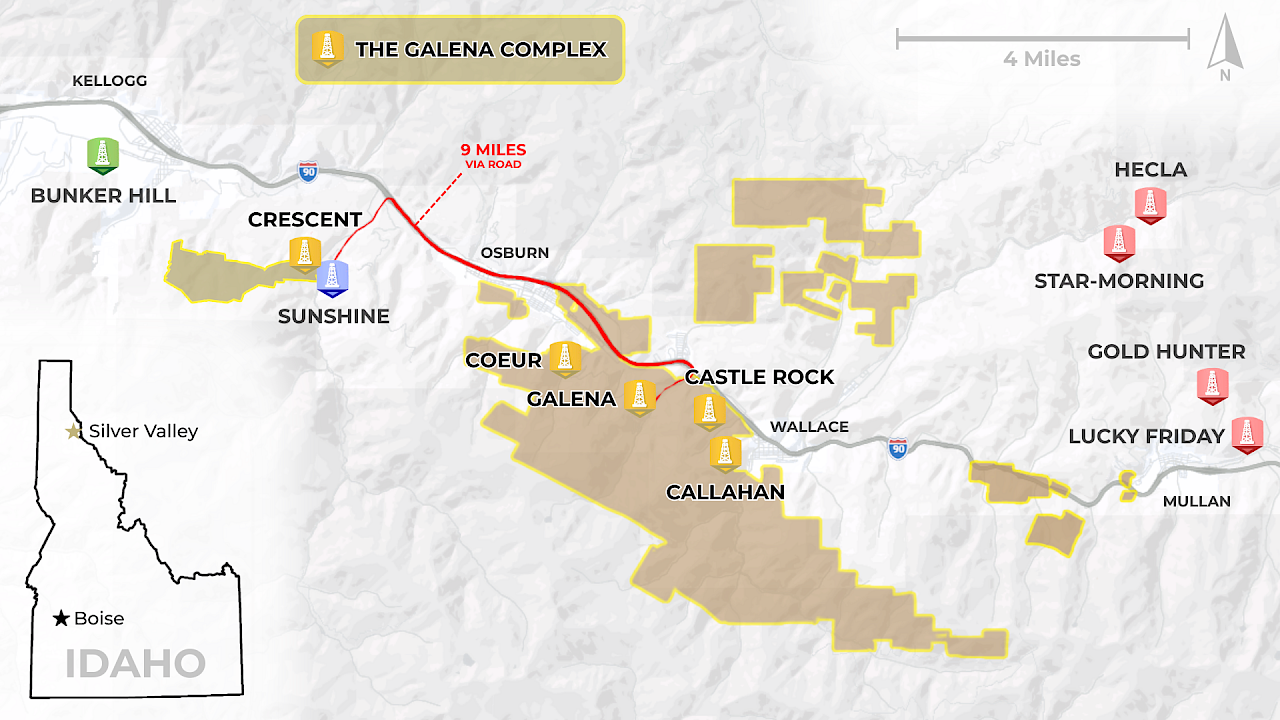

Americas Gold and Silver produces silver, copper, lead, and antimony from high-grade operations in the United States and Mexico. Its Galena Complex in Idaho is described by the company as a cornerstone U.S. silver asset and the nation’s largest antimony mine.

The company also formed a 51/49 joint venture with United States Antimony to build a new antimony processing hub at Galena, creating what it calls a U.S. “mine-to-finished product” antimony solution.

That phrase matters.

Mine-to-finished product is procurement language.

For a defense manufacturer scaling drones, sensors, munitions, rocket systems, and autonomous hardware, that is the type of upstream node worth reviewing.

The Galena data backs up the story. Americas’ May 2026 presentation states that Galena is the largest active antimony mine in the United States, produced about 561,000 pounds of antimony in 2025, has produced more than 20 million pounds of antimony since 2001, and has achieved 99%+ antimony recovery to concentrate grading.

Then the company cleaned up its capital structure.

On May 22, Americas announced an agreement with Sprott Mining Inc. to terminate the remaining 592,000-ounce silver delivery obligation, removing more than $45 million in variable future debt obligations.

USAS / PR

Release Routing Desk

Agreement with Affiliate of Royal Gold to Settle Fixed Gold Delivery Obligation

On May 26, Americas announced a second agreement with International Royalty Corporation, an affiliate of Royal Gold, to settle a fixed gold delivery obligation covering 8,861 ounces of gold. That removed more than $40 million in variable future debt obligations.

Combined, Americas says it has eliminated more than US$85 million in variable future debt obligations.

That matters for a potential offtake partner.

A serious buyer does not only look at geology. It looks at delivery risk, capital structure, operating control, processing plans, and the ability to reinvest into production.

For Anduril, the better read is simple:

- A U.S.-linked silver and antimony producer just removed old claims on future metal.

- Galena is being positioned as a U.S. silver-antimony supply-chain asset.

- The U.S. Antimony joint venture creates a possible domestic processing route.

That is not a stock-market footnote.

That is a supplier-screening event.

Then, on May 26, Americas Gold and Silver announced a second major cleanup. The company reached an agreement with International Royalty Corporation, an affiliate of Royal Gold, to settle its remaining fixed gold delivery obligation. That obligation covered 8,861 ounces of gold between June 2026 and December 2027. Under the deal, Americas will deliver 5,000 ounces of gold and issue 2,652,532 common shares at a deemed price of US$5.86 per share.

The company said the Royal Gold affiliate settlement removed more than $40 million in variable future debt obligations. Combined with the Sprott silver agreement, Americas said it has eliminated more than US$85 million in variable future debt obligations.

That matters for a potential offtake partner.

A serious buyer does not only look at geology. It looks at delivery risk, capital structure, operating control, processing plans, and management’s ability to reinvest into production.

For Anduril, the better read is this:

- A U.S.-linked silver and antimony producer just removed old claims on future metal.

- Its largest shareholder chose more equity exposure instead of holding the silver stream.

- The company reduced future cash obligations tied to legacy deals.

- Galena is being positioned as a U.S. silver-antimony supply-chain asset.

- The antimony joint venture creates a possible domestic processing route.

That is not a stock-market footnote.

That is a supplier-screening event.

The Smart First Step Is Quiet

Anduril does not need a press release tomorrow.

It needs an internal file opened.

The first move is technical:

- Qualify Galena antimony material

- Review USAS silver and antimony supply pathways

- Map the U.S. Antimony joint venture into a defense supplier framework

- Assess mine-to-finished-product traceability

- Model multi-year offtake options before defense demand gets louder

That is how a serious defense company gets ahead.

Anduril is already building the software layer.

It is already building the factory layer.

It is already building the weapons layer.

The next layer is the mineral layer.

Americas Gold and Silver now sits in a place that should be difficult for Anduril to ignore: a North American silver producer, a U.S. antimony producer, a company cleaning up legacy metal obligations, and a miner building toward a mine-to-finished antimony solution at Galena.

If Anduril is serious about building the arsenal, it should also be serious about the metals that arsenal depends on.

And USAS belongs in that conversation now.

And USAS belongs in that conversation now.